The Most Undervalued Miner in North America

There is a miner in North America that is flying largely under the radar and is still incredibly undervalued after a recent runup. Due to new catalysts, it should also be considered a major acquisition target for larger mining companies. I wanted to share this company and my thoughts with the great readers of Geiger Capital. Let’s dive in…

In my 2026 Market Outlook posted back in December, I mentioned a small-cap mining company that subscribers should keep an eye on. It’s name is Doubleview Gold Corp ($DBLVF). Entering the year they were waiting for an updated Mineral Resource Estimate (MRE) and Preliminary Economic Assessment (PEA) for their flagship "Hat Project" deposit in British Columbia.

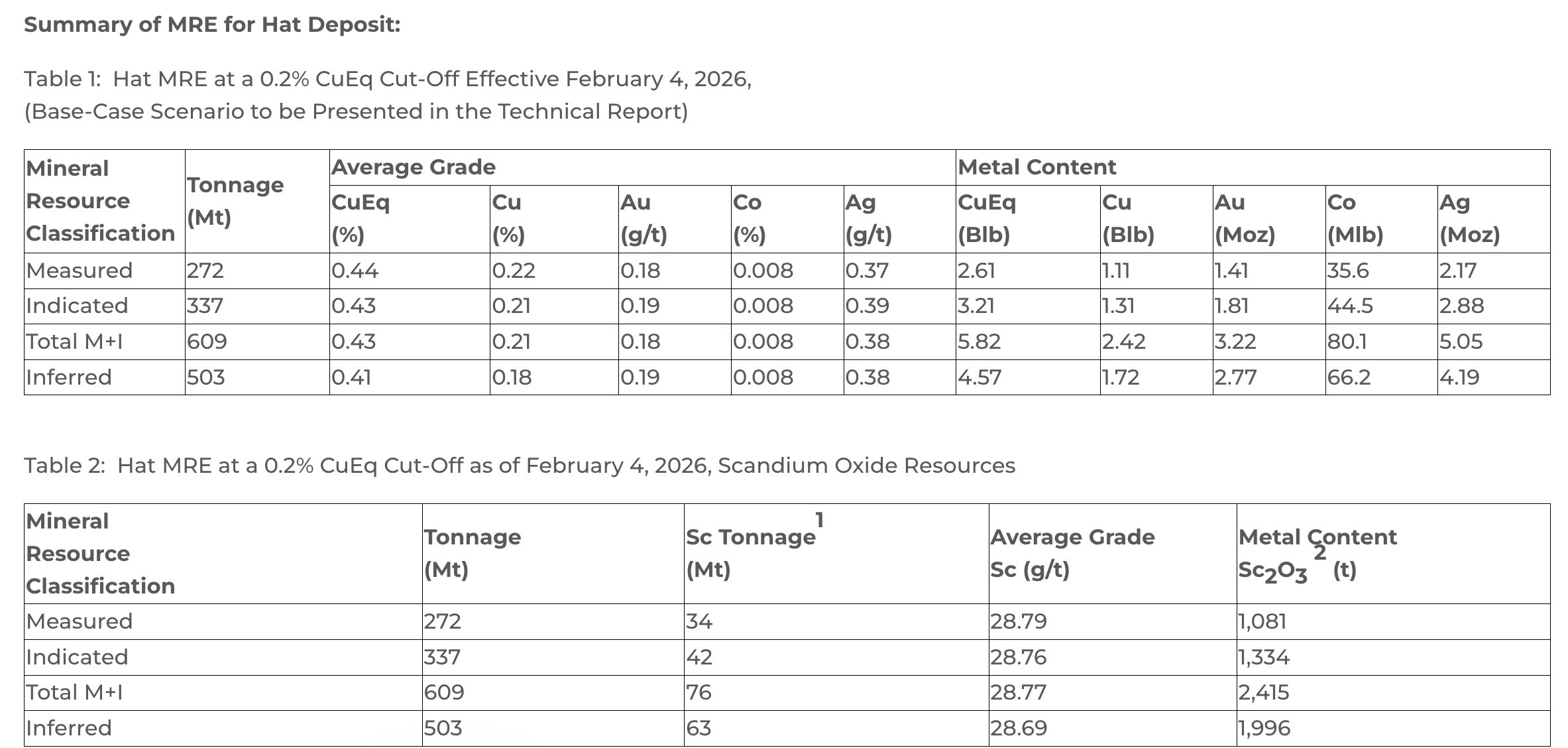

Early research showed that this large-scale deposit was a major source of Copper, Cobalt, Gold, Silver, and even Scandium. Copper and Cobalt are in high demand lately due to AI data centers, wiring, EVs and batteries. Gold and Silver are in high demand due to both geopolitical and monetary uncertainty. Scandium is a rare earth metal used in planes and military tech that was recently included on China’s export list. Most importantly, the company owns 100% of the Hat Project and it’s located in a mining-friendly part of Canada known as the "Golden Triangle".

From my post in December:

Well… that was correct and the stock is now up +140% YTD.

In late February Doubleview released their updated MRE and as predicted it was a very positive update. The measurements at their flagship deposit had grown substantially in size and confidence level, while also maintaining reasonable grades. For a junior miner/developer this was a key moment that helped de-risk the Hat Project meaningfully and immediately positioned it as a leading multi-commodity asset in a great location.

Then, just a week after the MRE, Doubleview announced the new Preliminary Economic Assessment (PEA) for the Hat Project on March 2nd. Even though the stock has pulled back a bit since, it was fantastic.

The assessment found that at "consensus analyst" metal prices, the after-tax Net Present Value (NPV) of the deposit is C$5-7 Billion. This is using extremely conservative price estimates. At current spot metal prices (as of late February in the assessment) the NPV would be C$11-14.5 Billion, more than double. Even the most conservative estimate is absolutely massive for a junior miner that is currently trading at a ~$400M market cap.

Looking at the mineral production estimates, the assessment said the Hat Project could be expected to produce an average of:

Copper ~75,000+ tons/yr

Gold ~250,000+ ounces/yr

Silver ~376,000+ ounces/yr

Cobalt ~2,700+ tons/yr

These are the annual production estimates of the project over the first 10 years.

It’s worth noting that the projected Cobalt production of ~2,700 tons per year would be equivalent to ~65% of North America’s entire Cobalt production in 2024. This mine would immediately become a primary North American source for both Cobalt and Copper.

This study is incredibly bullish, and again, very conservative. It uses safe assumptions, much lower prices than spot and also includes buffers for unexpected costs. It’s baseline almost entirely leaves out the bonus upside of Scandium, which could be 120+ tons per year. That is pure upside that could result in billions of extra value. Global demand for Scandium is estimated to 5-10X over the next decade due to growing commercial and military applications. The problem has been securing reliable supply due to most of it coming from China and Russia. The Hat Project could now be a major North American source, and it is barely being reflected in this NPV.

Here is what the CEO of Doubleview Gold said following these PEA results:

After this PEA the company is immediately moving into a Pre-Feasibility Study (PFS), providing a clear roadmap for early works and permitting activities later this year and into 2027. Doubleview is trading well below it’s peers and the Hat Project appears extremely undervalued even at the "consensus" estimates.

The market has not realized what this PEA has shown or what the Hat Project may become for North America, as both Canada and the US race to secure domestic mineral supply chains. In addition, I believe there is now a very high chance that a larger miner comes in and makes a buyout offer. The PEA de-risked the project while also leaving a lot of potential upside. This could be one of the largest, most valuable developing mines in the world that is not already owned by a major mining company or a nation state.

In early January, I told our subscriber chat that I had initiated a small position in $DBLVF and today I am still holding the entire position up ~140%. I believe this company is very undervalued following the Hat Project PEA and it should see significant upside even without a buyout. However, I think an acquisition is now extremely likely in the coming months/quarters and the stock has the potential to go up multiples from here.

*This is a small-cap company. Do your own research.

As always, this is not financial advice. I am sharing my personal views. It is meant to stimulate ideas and is not investment advice. Make your own decisions.

So the problem with this project is that Canada is nearly uninvestable. I live in BC. These days, a big chunk of everything has to be GIVEN to First Nations or your project will get blocked. They might decide to block it anyway. Then there is the ever changing regulatory climate. Enbridge CEO echoed similar sentiments recently.